2025 Annual Letter

Tensions, tensions everywhere and not a datum to believe

“I was on an airplane and there was internet – high speed internet – on the airplane. That is the newest thing that I know exists. And I am sitting on the airplane and they go, “Open up your laptop; you can go on the internet.” It is fast and I am watching YouTube clips. I mean I am in the airplane! And then it breaks down. And they apologize, “The internet is not working.” And the guy next to me goes, “This is bullsh*t” Like how quickly the world owes him something he knew existed only ten seconds ago.”

Louis CK, “Everything is Amazing and No One is Happy”

The above quote easily applies to today’s sentiment around generative AI. Transformer technology has already been taken for granted, while attention has shifted to general-purpose robots and the promise of multi-chain, agentic workflows.

Public awareness of private, venture-backed companies is at an all-time high. Investment banks are initiating equity research coverage on SpaceX, crossover funds are re-emerging alongside a renewed push from banks to “democratize alternatives.” Investors are fearful of missing out on what are framed as once-in-a-generation private market opportunities.

However, we are also acutely aware of the boom-and-bust dynamics of financial markets—dynamics that are amplified in venture capital, where pricing is infrequent and far less transparent than in public equities. The return of “venture tourists” echo 2021 - 2022 phenomena and it is more likely than not to end the same way: concentrated bets through multi-layered SPVs performing worse than the S&P 500, even before inclusion of an illiquidity premium. If we start seeing SPACs again, run.

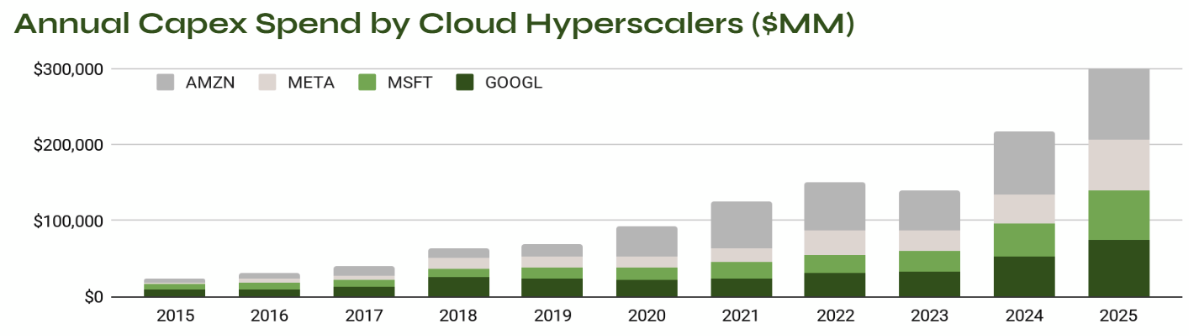

At the macro level, it is clear we are in an AI investment supercycle. Private enterprises have invested at least $820BN in Capex and R&D over the past year, with investment spending expected to grow by +34% over the next 12 months. For a sense of proportion, that $820BN number is greater than the annual GDP of 170 of the 195 recognized countries on earth. 90% of that spend is concentrated among a few US based hyper-scalers:

Numbers like this naturally spark concern. Can these companies afford to spend so much on AI infrastructure? Well, the benefit of being a part of a sprawling, globally dominant organization is the ability to absorb spend within diversified revenue streams; Google has Search and Youtube, Amazon has a direct relationship with 90%+ of US households. Placing investment spend within the context of company size, our concern lessens slightly:

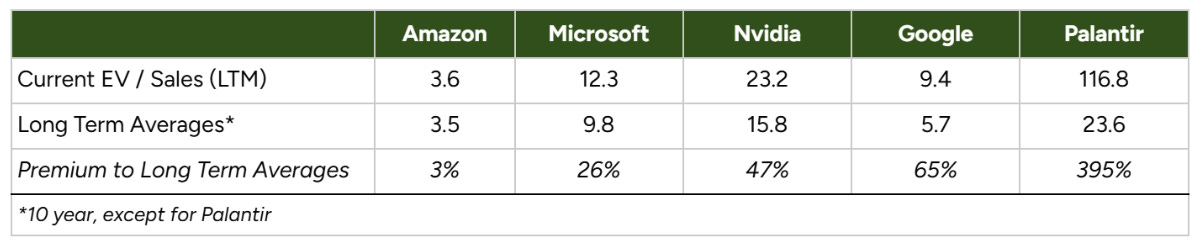

Despite the cash buffer, valuations relative to historicals appear a bit stretched among hyperscalers and AI stalwarts. Pockets of exuberance need to be edited out of any peer sets when evaluating exit comps.

More concerning is how dependent national economic growth has become on continued AI investment. In the first half of 2025, Pantheon Macroeconomics found that AI‑related spending contributed around 0.5 percentage points to U.S. GDP growth. They estimate that GDP would have grown at a mere 0.6% annualized rate in the first half of 2025 were it not for such spending. 50% of our total economic growth was investment from a handful of firms.

The Trump administration, along with support from Big and Small Tech, have framed AI Accelerationism within the context of global competition. They state that, if we do not adopt and accelerate these technologies faster than China, we will lose our place as the dominant superpower and be subjugated to the East in all forms of doomsday-war scenarios. Progressive and conservative leadership in the US have found equal footing on the matter, which should be cause for celebration, since they agree on little else. But free market capitalists should be loath to cheer on the US government taking 10% ownership of Intel and the US Secretary of Commerce stating they want to do it more often. Competing with China looks more and more like mimicking their protectionist industrial policy.

The increasing interconnectedness between tax-payer dollars and speculative AI spend draws comparisons to the “Too Big to Fail” dynamics of 2008, particularly among the largest venture-backed AI model builders: OpenAI, Anthropic and xAI. We have never lived in a time when pundits seriously debate whether a company will IPO at a trillion-dollar valuation or collapse into bankruptcy. In 2026, we expect all three companies to flesh out their business models and more clearly communicate their paths to profitability, as investors are becoming increasingly wary of the future burn needed to stay ahead in this AI arms race.

Five Signals over a bunch of noise

I thank whatever God (s) (or the void for atheists) that I do not have to write up a weekly market recap, attempting to draw some type of cohesive narrative from quadrillions of individual decisions and algorithmic trigger points. As humans, we crave narrative to make sense of the world, and financial gurus schill ’em out over mainstream news outlets and social media with such unabashed confidence.

But we should not be blind to the events of the year, and with enough time and thought, we can identify signals amid the noise; more glacial movements that are unlikely to change course into 2026 (until they do?). These signals are developed in collaboration with The Economist.

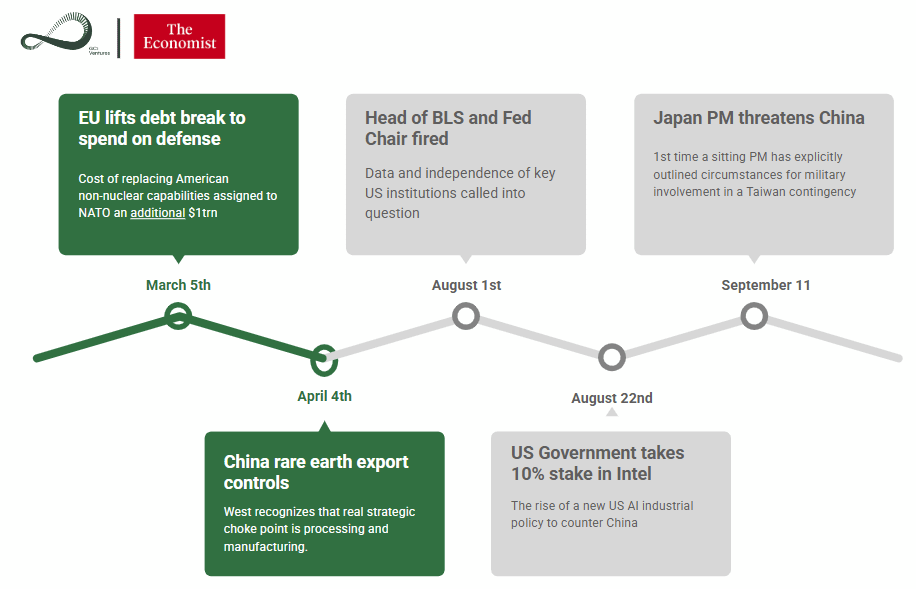

US economic data has been a mess this year, impacted by DOGE-related layoffs at data collection agencies and the longest government shutdown in US history. The firing of the head of the Bureau of Labor Statistics in August drew almost universal scorn from political pundits, investors and citizens, sparking concerns of massaged data to shape a political message. Lack of data transparency comes at an extremely tenuous time, when US monetary policy is being guided by monthly inflation readouts. Fed Chair Jerome Powell indicated skepticism toward the Oct-Nov data, implying that December’s "clean data" will hold more weight in future policy decisions. As of late December 2025, the publication of third-quarter GDP readings has been delayed, leaving markets waiting for official growth figures.

Despite data murkiness the Fed went ahead with interest rate cuts anyway, though consensus among governors is at an all time low. Adding to uncertainty around the path of the dot plot is the upcoming appointment of a new Fed Chair - one that may be more pliable to the Executive Branch’s bidding. “Fake news” could extend into “Fake Data” as cover for politically motivated monetary policy.

Elsewhere, in Europe, populist and far-right parties have made notable gains amid persistent voter concerns over the cost of living, growth, and migration. At the same time, the U.S. questioning the reliability of NATO’s security guarantee have amplified European debates about building a more independent security posture. Populist leaders often fold these arguments into a broader sovereigntist agenda, emphasizing national control and reduced external constraints as core components. While Germany has eased its debt brake for defense, other Euro area member states face high public debt and Excessive Deficit procedures, which may limit their ability to match spending increases.

Simultaneously, more and more countries seem to be praising the economic strength of China. This year showed the power of China’s industrial chokeholds. China’s share of the world’s manufacturing value added exceeds one-third, giving it the power to disrupt global supply chains overnight. In April, Xi Jinping’s restrictions on rare-earth exports are one example of how China can use other countries’ dependency as a weapon. DeepSeek showed what China can do in artificial intelligence, despite America’s best efforts to hobble it. In response Western democracies have moved for more direct control of their industrial titans, raising the eyebrows of free-market capitalists.

Eyebrows were also raised (and began to drip sweat) in the Far East as Japan got its first female prime minister. Takaiche Sanae is described as the country’s Margaret Thatcher and appears to have the same proclivity for controversy. Prime Minister Takaichi made unprecedented remarks suggesting that a Chinese naval blockade of Taiwan could constitute an “existential threat” to Japan. This framing is significant because it provides the legal justification under Japan’s collective self-defense doctrine to deploy its military to support friendly nations. Analysts note this is the first time a sitting Prime Minister has explicitly outlined circumstances for military involvement in a Taiwan contingency. To support this stance, the administration has pushed for revisions to Japan’s “three national security documents” and reportedly prepared to deploy missiles near Taiwan. The remarks have severely strained relations between Tokyo and Beijing, with China claiming Takaichi “crossed a red line. While Japanese business interests are privately counseling a more dovish approach, most analysts view this as a “critical tension” and the most consequential development for the 2026 regional outlook.

Tensions, tensions everywhere and not a datum to believe

What binds these threads together is not a single narrative, but the growing fragility of the systems we rely on to interpret reality itself. AI optimism coexists with venture excess; industrial policy masquerades as free-market competition; central banks act amid compromised data; and geopolitical red lines are drawn in public even as economic interdependence deepens. Everywhere there are tensions between growth and discipline, security and openness, innovation and speculation, yet fewer reliable data points with which to anchor conviction. In such an environment, the greatest risk is not missing the next technological supercycle, but mistaking momentum for inevitability and narrative for signal.